|

|||||||||

7. Estimation of commercial vessel depreciation and value based on cost approach

MV = RC×(100 %–D2)/100 %×(100 %–D4)/100 %×(100 %–D5)/100 %–(D1+D3). |

(7.1) |

Physical depreciation grows out of normal ageing of the commercial vessel (or other asset of the marine company). Such kind of depreciation can be removable or irremovable.

The removable physical depreciation can be characterized by the necessary expenses on forthcoming routine repair and maintenance which the owner should incur for profit maximization.

The irremovable physical depreciation characterizes value reduction over the time with the account the limited life time of the commercial vessel or other real asset of marine company.

It is necessary to note the following specific feature of marine commercial vessels as objects of deterioration estimation. According to existing convention of shipbuilding and shipping which are established by survey–inspection services of the various states (see item 1.4) exercising the control over safety of shipping and human life protection at the sea, the vessel should correspond to a certain strict enough set of requirements, otherwise her operation in the sea is impossible, and the owner cannot receive the profit. The vessel value thus accordingly cannot exceed the scrap value.

The specified earlier (in the article 1.4) organizations monitor periodically that the vessel meets the requirements.

From the formal point of view the requirement of the specified organizations cause the necessity of operating repairs, so the removable physical depreciation D1 of a commercial vessel, and the same requirements, to be exact their changes, predetermine in many cases removable functional depreciation D3 (that is the general removable depreciation D1 + D3 in aggregate).

Except requirements of the inspection organizations, the removable physical depreciation can be caused by the necessity of restoration of the structures lost at failure, systems and devices, and also these structures or systems which are not connected with the safety of shipping and are not inspected, but their existence on board is necessary for characteristics to be in conformity with the project data for which the replacement cost RC and further the market value MV is determined according by the cost approach.

Vessel repair includes a complex of technical operations aimed at restoration of serviceable or efficient condition of the vessel hull, devices, systems, equipment or mechanisms, including their replacement, and also general functional suitability and seaworthiness of the commercial vessel.

Unlike the repair, at reconstruction the characteristics of the commercial vessel are change, instead of being restored.

Investments into the repair and vessel maintenance service are limited by the necessity to bring the vessel into an efficient and seaworthy condition according to operating rules and are not a way of vessel value accumulation, and serve to decrease investment risks.

Further investing after restoration of seaworthiness and functional suitability according to specifications of an efficient vessel is not an increase of her value, unlike possible investing in reconstruction that causes functional characteristics of commercial vessel to change.

Functional depreciation is usually characterized by depreciation owing to designing faults. Depreciation of this kind also can be caused by age factors, for example the external obsolescence of used materials or accessories in constructing. Such can be either removable or irremovable.

Commercial vessel elements with irremovable functional depreciation can be subdivided in to two groups referred to either redundancy or insufficiency of the given element.

Functional depreciation D3 and D4 does not influence the value of the commercial vessel or other real asset of the marine company and is equal to zero if the replacement cost RC is used as a basis for evaluation based on cost approach namely the functional analogue having the same functional drawbacks.

External obsolescence of the commercial vessel or other real asset of the marine company D5 (the economic depreciation) characterizes the reduction of value caused by the influence of external factors, such as the general decline of the market, the decrease in economic activity.

External economic obsolescence of the vessel D5 and usually the functional depreciation D4 have irremovable property.

The general recommendations concerning the application of the depreciation estimation methods of commercial vessel or other real asset of the marine company of listed types are follows:

– Removable depreciation (physical D1 and functional D3) should be estimated by the method of subdivision into the integrated groups on the basis of the data about the reproduction cost structure, that, in turn, influences the choice the method of reproduction cost estimation, using the advantages of its estimation as the total costs as opposed to the methods based on comparable sales;

– Irremovable physical depreciation D2 of the commercial vessel can be evaluated by the «life time» method, thus the important task here is to estimate the life time, for example, with the account profitability and actual years of not a new vessel or other real asset of the marine company and the kind of depreciation to vessel age proportion (the linear proportion or other);

– Irremovable functional D4 and external D5 depreciation of commercial vessel or other real asset of the marine company should be estimated by the method of income loss capitalization, thus it is necessary to define the loss of the income caused by the influence of the evaluated element of inefficiency, or based on comparable sales approach, if there is an analogue, which for the named depreciation is known (or evaluated).

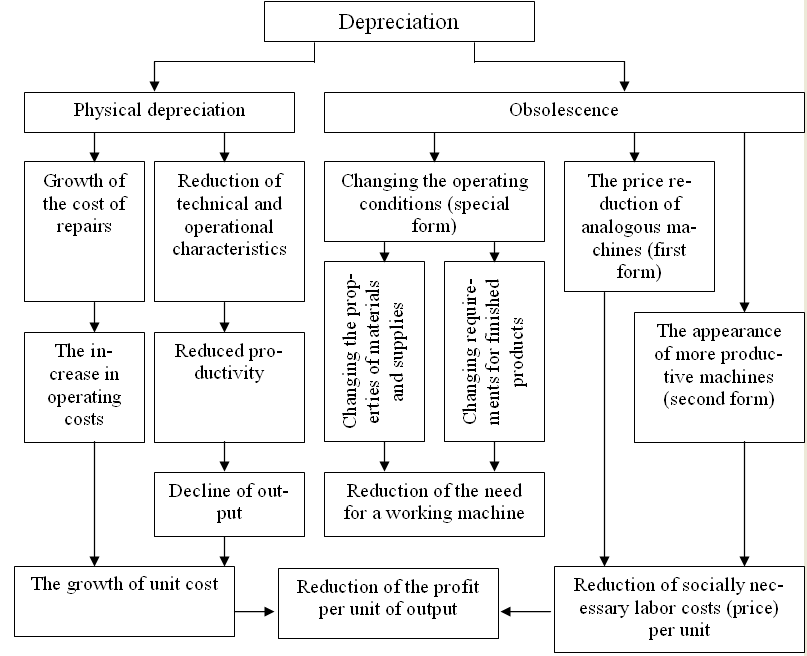

Figure 7 shows the widespread classification structure of depreciation indicators for technical and economic estimations in shipbuilding and shipping.

Studying the classification structure makes it possible to arrive at a conclusion, that for the correct estimation concepts of classification of the indicators corresponding to the valid factors of depreciation have the most essential value so that the sum of the terms corresponded to the general economic index of depreciation are more important rather than the specific share of depreciation economic index into the elements which can differentiate in various expert works at presence that of the bases.

It should be added that in practice of fleet technical operation the deterioration is one or another dimensional physical indicator of deterioration, for example loss of metal plating thickness caused by corrosion of the hull or total square of plating which is deformed and is subject to replacement instead of decrease of the value. It is necessary to consider, that technical deterioration of the commercial vessel is not a proportional correspondence to economic depreciation (that is value loss).

Test questions

1. Kinds of economic depreciation of the commercial vessel: external and internal depreciation, removable and irremovable depreciation.

2. General list of economic depreciation signs.

3. Concept of depreciation economic irremovability.

4. Reference of absolute estimation (monetary) to removable depreciation, and a relative estimation – to irremovable depreciation.

5. Vessel value estimation by the cost approach (the formula).

6. Rules concerning the vessel operating repair influencing the estimation of the removable physical depreciation.

7. Causes of commercial vessel functional depreciation.

8. External factors influencing commercial vessel value.

9. Recommended method of determination of commercial vessel removable depreciation (physical D1 and functional D3).

10. Recommendation concerning estimation of irremovable physical depreciation.

11. Methods recommended for estimation of irremovable functional and external economic obsolescence of the commercial vessel.

Fig. 7. The classification scheme of the depreciation performance common in shipbuilding industry and shipping