|

|||||||||

14. Economic model of cargo vessel

The account at the level of estimation of NOI usually is not provided for the marine company isolated asset. Concerning marine commercial vessels of the separate classes, which are used for efficiency increase of the marine company’s property complex, only expenses can be taken into account and the expenses records are not kept whereas other real assets generate income.С = СCR + СFED + СEXP + СSOC + СFL + СSUP + СRM+ СG + СMM + СDS , |

(14.1) |

where СCR – expenses for crew salary (labor costs); СFED – expenses for crew’s food supply; СEXP – the expenses for crew delivery; СSOC – specific payments to the social insurance funds of labor costs; СFL – fuel costs; СSUP – cost of supplies; СRM – operating repair and maintenance service expenses; СG – running costs; СMM – administrative expenses for management; СDS – marketing expenses.

Due to methodological reasons when estimating based on income approach the depreciation charges calculated by rules and standards of book keeping are not subject to inclusion in a set of operation costs and to subtraction from the annual income for estimation of the net operating income, though relative value of depreciation charges in shipping is rather considerable (from 20 to 40 % in relation to the operation cost of commercial vessel).

The annual operating expenses for crew support (СCR+СFED +СEXP), including expenses for crew salary (labor costs) СCR, and also for feeding СFEDand for delivery of crew СEXP(determined by the general rate of expenses for crew payment, except specific payments СSOC, for the off–budget funds calculated by standard rules) with the account operating standards and formed relations between the components makes approximately

СCR + СFED +СEXP ≈ (1,10 ÷ 1,20) × nЭ × сЭ, where cCR – the average annual expenses for support of one member of crew, nCR – the number of members of the crew, including, expenses for crew salary, are equal СCR≈ nCR×cCR.

The total rate of specific payments СSOCinto the off–budget funds from expenses for crew salary is determined by the components summation: for social insurance, for medical insurance, a pension fund, – and depending on specified terms can be specific payments from 32 to 40 %, on the average 36 % (in Russia).

The specific payments to the off–budget funds СSOCare equal approximately

СSOC≈ 0.36 × СCR ≈ 0.36 ×nCR×cCR.

The operational expenses for crew support including specific payments СSOCto the off–budget funds with the account the developed proportion besides the components СCR, СFED, СEXPand СSOC, is СCR + СFED + СEXP + СSOC ≈ 1.48 ×nCR×cCR.

The operational expenses for fuel and lubricants are determined as:

![]() ,

,

where РFL – the fuel stock on board (the expenditure of fuel during the voyage to be more exact, considering, that with commercial vessel characteristics rationality the expenditure of fuel during the trip usually corresponds with the specification fuel capacity); nR – the average number of trips within a year; ![]() – the cost of one tonne of the fuel used on the vessel vessel.

– the cost of one tonne of the fuel used on the vessel vessel.

The duration of cargo vessel round trip is determined as:

TRF=tR1+tR2+tG1+tG2+tM,

where tR1, tR2 – the running time during the trip to destination and return trip accordingly, tR1 = £ / (24 × υS1), tR2 = £ / (24 × υS2); υS1and υS2– the commercial vessel velocity during the trip to destination and return trip accordingly; £ – the extent of a trip line; tG1, tG2 – the duration of cargo operations in departure and arrival harbors tG1=PG×ηG1/qG1 and tG2=PG×ηG2/qG2; PG – the cargo capacity of commercial vessel; qG1, qG2 – the productivity of cargo operations in departure and arrival harbors; ηG1, ηG2 – the operating ratios of cargo capacity of the commercial vessel during the trip to destination and return trip; tM – the time expenditures for maneuvering.

The annual trip number is equal nR=TEXP/TRF, where TEXP – the duration of the annual operational period.

The statistical values of operational periodduration TEXP for cargo vessels in the published data [16] are at the average:

– For the universal dry–cargo vessel of deadweight to 6000 tonne – 341 days, with deadweight from above 6000 tonne – 337 days;

– For the dry–cargo vessel for transportation of mass cargoes (bulk) with deadweight to 20000 tonne – 336 days;

– For the bulk dry–cargo vessel of cement transportation with deadweight from 20000 to 50000 tonne – 334 days, with deadweight from above 50000 tonne – 332 days;

– For the dry–cargo vessel of wood cargoes transportation (for the timber and the kindling–wood) with deadweight to 7000 tonne – 339 days, with deadweight from 7000 to 15000 tonne – 338 days, with deadweight above 15000 tonne – 334 days;

– For the dry–cargo vessel for transportation of containers with deadweight to 6000 tonne – 336 days, with deadweight from 6000 to 20000 tonne – 336 days, with deadweight from 20000 to 30000 tonne – 334 days, with deadweight from above 30000 tonne – 333 days;

– For rolling cargo vessel with horizontal cargo operations (RO–RO) with deadweight to 40000 tonne – 337 days;

– For the refrigerator dry–cargo vessel with deadweight from 4000 to 8000 tonne – 336 days, with deadweight from 8000 to 20000 tonne – 335 days, with deadweight from 20000 to 30000 tonne – 332 tonne, with deadweight from above 30000 tonne – 330 days;

– For the lighter barge dry–cargo vessel – 333 days;

– For the barge carrier vessel – 335 days;

– For the ferry with deadweight to 4000 – 341 days, with deadweight above 4000 tonne – 337 days;

– For the oil tanker with deadweight to 6000 tonne – 340 days, with deadweight from 6000 to 20000 tonne – 337 days, with deadweight from above 20000 tonne – 332 days;

– For crude gase carrier with deadweight to 10000 tonne – 333 days, with deadweight from 10000 to 50000 tonne – 332 days, with deadweight from above 50000 tonne – 330 days.

The annual expenses for supply is equal approximately 7 % of fuel costs that is СSUP ≈ 0,07×СFL.

The annual cargo traffic is Q=PG×nR×∑ηGi, where nR– the number of trips within a year; ηGi – the operating ratio of the cargo capacity for the specification.

The annual income is determined by the formula I = Q × m, where m – the transport tariff rate – the cost of cargo unit (one tonne, one piece, unit of volume, etc.) delivery to destination.

The average annual charges for operating maintenance (the postponed expenses) are evaluated depending on reproduction cost RC or on construction cost of modern functional analogue of the commercial vessel.

The expenses for repair within a year make roughly 0.4 % from the reproduction cost of the vessel RС by data for marine commercial vessels [16, tab. 6П].

The close values of annual repair cost – about 0.8 % from reproduction cost of vessel RC – correspond to the analysis of the directory data [18, p. 62, tab. 3.1].

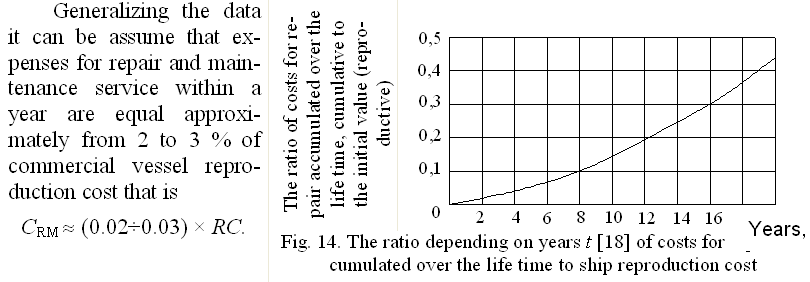

A little bit higher annual expenses for vessel repair follow from the analysis of the schedule presented in the directory data [18, p. 202, fig. 6] which is from 1.2 to 2.3 % on reproduction cost of vessel RС.

The figure below (fig. 14) shows the features of dependences between costs for repair accumulated over the life time and initial vessel value.

Test questions

1. Structure of cargo vessel operation costs of basic model.

2. Determination of the trip duration, the number of trips, the annual carrying capacity and the annual income.