|

|||||||||

18. General structure of the marine company’s property complex of assets and the organization of the marine industrial activity

The object of the evaluation and efficiency estimation of investments is the isolated asset or property complex (business, private capital) the marine company.

In accordance with the Federal law «The Appraisal activity in the Russian Federation», July, 29th, 1998 № 135–ФЗ to objects of an evaluation are included: the separate material objects (property); the set of goods consisting property of the person, including property of a certain class (equipment or real estate, including the enterprises); the property right and other real rights to property or separate goods of the property set; the rights of demand, the obligations (debts); the works, services, the information; other objects of the property rights in which relation the legislation of the Russian Federation establishes possibility of their involvement in commercial turnover.

According to the developed practice the objects of sale and purchase, pledge, rent and other contracts concerning the marine companies connected with an establishment, change and the termination of property rights, and also object of appraisal usually are: commercial vessel or other real asset of the marine company, the isolated property complex, a share of the right or a share holding, the enterprise as a whole or separate property (that is the rights concerning property), identified as the structured set as a part of the operating company, and in a specific case – as a single set consisting of one asset, the separate rights or servitude, etc.

The examples of sets which can be defined methodologically as assets of the marine company:

– The marine commercial vessel of a certain purpose and the characteristics, the separate right concerning commercial vessel;

– The equipment and a real estate, including, facilities of the marine company coastal infrastructure;

– The intangible assets, including goodwill – unidentifiable part of intangible assets associated with identified assets of the marine company, including intangible or (and) tangible;

– The packages of securities and Contracts for property turnover – of the identified property rights, including personified;

– The liabilities and rights concerning certain (identified) quantity of uncertain property.

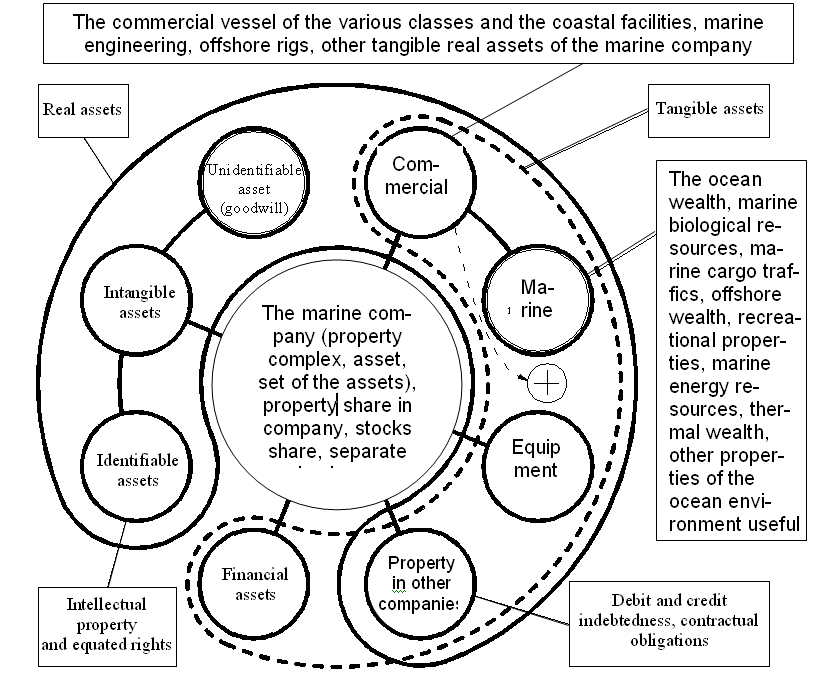

The structure of assets as a part of a property complex of the marine company is presented on the scheme

The property complex of company is defined as «all kinds of property intended for its activity, including the land plots, buildings, structures, equipment, stocks, materials, production, rights of demand, debts, and also the rights of the company to have a symbol individualizing the enterprise, its production, works and services (the company name, trade marks, service marks), and other exclusive rights unless otherwise provided by the law or the contract» (article 132 of the Russian Federation Civil code, Part 2).

The structure of assets as a part of a property complex of the marine company is presented on the chart (fig. 18.1).

Fig. 18.1. Assets as a part of the marine company’s property complex:

_ _ _ _ – outlined material assets; _______ – real assets, i.e. all assets, except for financial; – direction of investing the financial assets in the real assets carrying out the innovation part of the investment project, i.e. producing the non–identified intangible asset – goodwill and reproducing the value of the marine wealth

There is a following scheme of assets classification:

– Company (the property complex) as a form of generalization of assets;

– Financial assets;

– Marine vessels and marine engineering;

– Real estate, including natural resources;

– Equipment, devices and mechanisms;

– Intangible assets identified as intellectual property and property rights equal to it;

– Unidentifiable intangible asset – goodwill, including access possibilities to ocean resources, for example, to ocean biological resources or marine cargo traffics.

From the methodological point of view the industrial economy is a network of co–operating property complexes and general structure of each of them corresponds to the scheme. External interaction between property complexes is carried out on the basis of commercial contracts, and management and distribution inside of them has administrative character and is subordinated to interests of investors.

Assets of the marine company can be classified into the following sets: the financial assets and the real assets, the tangible and the intangible. All sets of assets are referred to real assets (tangible and intangible) except the financial.

The purpose of investing of the financial assets in sets of the marine company’s real assets can be:

– Generation of unidentifiable intangible asset – goodwill which is formed as a difference between the marine company’s property complex value and the sum of values of its separate identified assets that is as an added value in case of merging of real assets in structured sets – in case of gaining parts in whole, that by the formal point of view is the purpose of real assets property complex creation and the reason of its stability;

– Reproduction of the ocean resources value as difference between the value of property complex of the marine company which is the investor means of access to ocean resources and which depends on efficiency of ocean resources, and total value of investments into the marine company, that is the sum of value of financial investments and values of separate real assets.

Natural resources are a wider concept of economics, than ocean resources in aggregate properties of the marine environment which is the aim of investor’s interests. The natural resources, part of which are marine resources, also include other ones, such as territories, suitable for construction, soil and agricultural productivity, minerals of subsoil resources, fresh water resources, useful properties of materials, properties of ether to transfer the information in various ranges, climatic and natural advantages in certain territories, etc.

An abstract example concerning the property complex of the company based on use of real estate is the fact that unidentifiable intangible asset and natural resources (for example, occupied sites of territory) growing in value in process of recreating of «improvements» (real estate) have in many respects the close economic value.

So, when the real estate is located in a brisk place the value advantage of the property complex can be estimated dually rather as goodwill the company using loyalty of clientele in a crowded place, or as advantages in value of real estate as a part of the property complex of the company located in an expensive site of a busy place.

The estimation of ocean resources as a part of marine company’s property complex or as resources, associated with a certain real asset of the marine company, also has a close relation to unidentifiable intangible asset and is shown in the scheme of the marine company property complex structure (fig. 18.1).

The structured set of marine company’s real assets has the properties which are absent in other parts – in the invested real assets taken separately. The dialectic law of transformation of quantity into quality operates here. The value of the whole set should differ from the sum of values of the parts. The value of the marine company’s property complex is more than the total sum of values of separate assets for a size of the unidentifiable intangible asset – goodwill.

And bankruptcy of the company can mean exhaustion of unidentifiable intangible asset that will lead to re–structuring of the property complex and sale on assets if the sum of parts values becomes more the value of the property complex. The similiar reason – the loss of the value of an occupied territory site owing to inefficiency of the superstructure – will lead to its liquidation.

The property complex of the marine company (the definitions – «maximum» and «minimum») methodologically can be defined as:

– Set of the invested real assets and the produced unidentifiable intangible asset corresponding to the value influence of ocean resources and associated with the set of invested assets, that is as a set of the properties presented in parts, and the properties which are arising in case of combining the parts and which are absent in parts taken separately (in separate real assets);

– Unidentifiable intangible asset in case of combining the associated with a set of the invested assets that is as the additional properties arising parts (real assets in the structure) except the properties presented in separate parts.

Concerning financial assets (sums of money as a part of a property complex) it is should be explained, that the characteristic is a nominal sum of money.

The subject of an applied economic estimation is to estimate the market value or other value of the object, that is, estimation of real assets in terms of financial assets. Thus the value of financial assets is equal to the face value.

The characteristics of marine company assets are identification signs or associative signs with identified assets for unidentifiable assets. Other characteristics are secondary; they are particulars of identification signs – primary characteristics of assets.

The investment project includes innovative and financial stages that influence the estimation of investment risks.

The analysis of the classification structure of assets as a part of the marine company’s property complex (fig. 18.1) allows to define the investment projects types (or the stages of the investment project):

– Innovative project, when investment of financial assets is made in real assets of the marine company (tangible and intangible) for the purpose of value growth of the set of real assets bought separately;

– Financial investment project as receiving of financial assets in the form of profit in process of productive operation and sale of real assets.

The greatest risks correspond to an innovative stage of the investment project – an initial stage when profit is reinvested in real assets and during which the value of the marine company’s property complex is rather insignificant, that is, the relation of profit to the value of the business, associated with cumulative commercial risks is great, and the value of the property complex is insignificant in comparison with the profit concerning the characteristic industrial proportions, but is characterized by growth.

At the innovative stage of the investment project the asset that has the greatest influence on the value of the marine company’s property complex is an unidentifiable intangible asset – goodwill, which is an estimation of innovative strategy of the investor of ocean resources development.

The implementation of investment projects of the innovative stage in marine industrial activity, that is innovative activity, is made by joint efforts of investors, hired workers, and first of all highly skilled experts, authorities and the government.

The financial stage of the investment project on receiving of financial assets in the form of profit or in case of sale of real assets, that is the financial investment project is characterized by less commercial risks that testifies, on the one hand, the exceeding of the business value in relation to the profit, on the other hand, the smaller profit (profitableness) in relation to the capitalization of the marine company at the financial stage of the investment project.

Thus, receiving of profit in the financial form is provided at the expense of depreciation of the set of the marine company assets and transformation of a property complex in the financial form that means the tendency of industrial turning.

The specified processes lead to reduction of commercial risks and profitableness to zero, and the value of the property complex of the marine company in process of realization of the financial project becomes equal to the total sum of values of the assets sold separately.

Finally, the financial stage of the investment project usually is followed by bankruptcy and liquidation of a property complex (sale on assets) if effective management which should be capable to give a new innovative strategy is not applied and to show the investors other ocean resources available for development.

The economic estimation of the relative value of the marine company’s property complex, that is of a parity of the marine company value and the values of its isolated assets, and also the value of separate functional property complexes as a part of the marine company is of interest.

The question is if it’s economically more reasonable to combine selected functional property complexes in a single marine company or it’s better to form property complexes as independent companies.

The advantage concerning small marine companies, whose isolated assets or separate property complexes in value are proportional to the enterprise as a whole, is that the financial result is more available to investors (participants – owners).

The practice of market reforms in Russia shows the tendency of re–structuring of the large marine companies and isolation of participants. This tendency is characteristic in case when the state doesn’t take part in this process.

It should be noted, that re–structuring of the large marine companies and isolation of functional property complexes to a certain extent is a progressive process of advancement of investors to the property that in reasonable limits corresponds to the increase of economic efficiency of the marine companies, property complexes and assets.

In the methodological relation the tendency of isolation of functional marine company’s property complex in which structure there can be single real assets proportional in value to a property complex, in particular marine commercial vessels, is one of the reasons of the specified feature.

It should be added, that large marine companies, as sets of several functional property complexes, in spite of the fact that they are characterized by difficulty of access of investors to financial result (for example as joint–stock companies uniting numerous investors – shareholders), can be not only the result of a purposeful policy of administrations on protection of their integrity, but also the result of locally formed conditions of prevalence of demand over the supply or surplus of resources.

Usually it is not a long–term factor, so the probability of re–structuring of the large marine company therefore remains and small enterprises can be considered as steadier.

For example, opening of a perspective offshore deposit and formed surplus of resources for development can be a reason of establishing the joint–stock company which will accumulate funds by issuing shares of stocks and grow fast, though the access of a considerable quantity of shareholders to financial result of the company will be complicated.

In view of the fact, that for capital–intensive industries to which the marine companies, in particular, belong, can be characterized by the unbalanced market and the lag between supply and demand is, that, by the way, it is peculiar for shipbuilding at the beginning of the XXI–st century too there can be temporarily formed the conditions when integration of the shipyards (or integration of the shipping companies provided that there is a great demand in transport or fishery shipping) becomes rather reasonable.

At the same time, when there is no government policy concerning support of the large innovative enterprises, small marine companies (usually in the form of limited liability companies) with separate assets in their structure, whose value proportional to the value of the whole company proved to be more stable economically.

And this is one of the most important features of the marine business underlying pricing from the point of economic methodology, along with other important features including the orientation to development of ocean resources and original system of external and internal communications: industrial, technological, functional, etc., as well as global international economic relations.

Test questions

1. Object of evaluation – the property complex or the isolated asset of the marine company.

2. Sets which can be methodologically defined as assets.

3. Standard definition of the property complex.

4. Classification of marine company assets.

5. Tangible and intangible assets.

6. Financial and real assets.

7. Purpose of investing the financial assets into real assets.

8. Methodological concept of the property complex.

9. Subject of appraisal.

10. Identification signs of assets.

11. Concept of intangible assets.

12. Kinds and stages of investment projects in view of classification of assets: the innovative project and the financial investment project.

13. Commercial risks at an innovative stage of the investment project with the account the capitalization of business.

14. Business value and risks in process of implementation of financial investment project.

15. Features of the marine companies underlying pricing from the point of the economic methodology.

18.1. International specialization in shipbuilding and shipping

In connection with global processes of technical improvement of the commercial vessels designs, accompanied by complication of technology and accumulation of assets value of shipbuilding industry, and also due to increased prices for resources and labor there is an un–surge in prices for shipbuilding manufacturing and the prices at the second–hand market of commercial vessels. The rise in prices proceeds, despite the growth of volume of shipbuilding output and the general phenomena of crisis in economy.

According to the consulting company Clarkson Research Service, the volume of release of shipbuilding tonnage output in 2005 has reached 27.5 million CGT (Compensated Gross Tons), or 69.3 million tonne of deadweight.

The average size of capital investments per tonne of cargo vessel deadweight is 1.1 thousand US dollars that roughly corresponds 2.0 thousand US dollars per tonne of displacement empty.

To a greater extent these data characterize investments into construction of batch large–capacity crude carriers, bulk cargo vessels, container vessels and vessels for transportation of the liquefied gas, having the greatest total displacement and deadweight – about 95 % from total values of displacement and deadweight of marine cargo vessels.

Growth of capital investments in world shipbuilding more than twice from 2000 is caused not only by growth of the shipbuilding output, but also by general increase in cost of shipbuilding tonnage. Distribution of investments into construction of cargo vessels looks as follows: container carriers – about 36.5 % of all investments, crude carriers – 29.0 %, gas carriers – 16.0 %, vessels for transportation of bulk cargoes – 13.6 %.

In numerous researches published by the research organizations and consulting agencies show the data on the contemporary global shipbuilding market of marine cargo vessels.

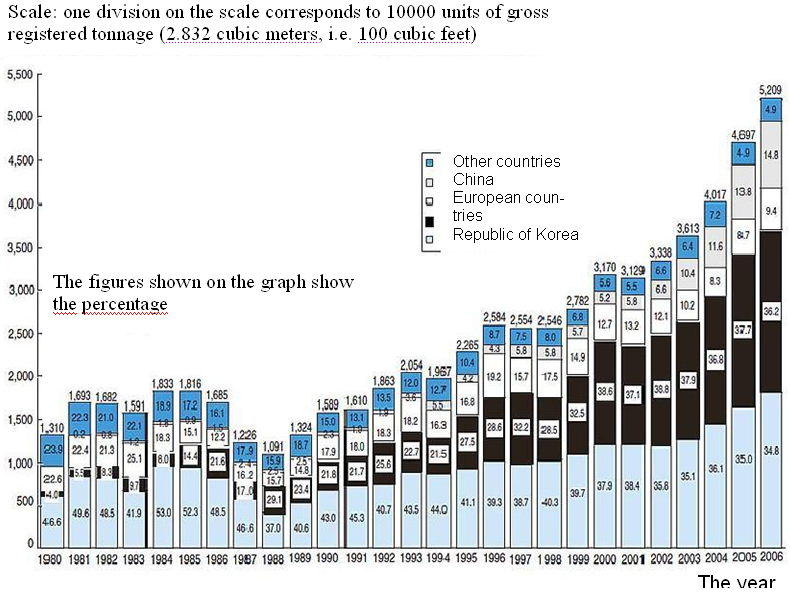

The diagram (fig. 18.2) shows the dynamics annual output growth of the marine commercial vessels manufacture (according to the data of: Report on Marine Affairs. Maritime Bureau, Ministry of Land, Infrastructure and Transport,

http://www.jpmac.or.jp/english/report_on_maritime_affairs/index.html.)

Fig. 18.2. The growth and structure of manufacturing of marine commercial vessels completed by the specified year in the world

At the beginning of XXI century more than 90 % of marine commercial vessels tonnages are manufactured at the shipyards in the countries of Pacific Rim. The general tonnage of the vessels manufactured in Republic of Korea in 2005 is about 37 % of all world shipbuilding industry output. The second place by the manufactured vessels tonnage is occupied by Japan – 30 %, the third – by China (13 %).

The manufacture output in the European states in relation to the world output can be characterized as follows: Germany – 4.1 %, Poland – 2.0 %, Italy and Croatia – round 1.5 %, Turkey and Denmark – about 1.1 %.

The leader among the states marine manufacturing commercial vessels is the Republic of Korea. Shipbuilding orders for its shipyards in 2006 have made half of orders in the world.

There was a following world distribution of output the volume of in first ten shipyards (where the shipyards of the Republic of Korea occupy fro the first to the seventh places):

1. Hyundai Heavy Industries;

2. Samsung Heavy Industries, united with company–contender Daewoo Shipbuilding and Marine Engineering Co.;

3. Daewoo Shipbuilding;

4. Hyundai Mipo Dockyard – the branch of Hyundai Heavy Industries;

5. Hyundai Samho Heavy Industries – the branch of Hyundai Heavy Industries;

6. STX Shipbuilding;

7. Hanjin Heavy Industries and Construction Co.;

8. China's Dalian New Ship Heavy Industry Co., China;

9. Shanghai Waigaoqiao Shipbuilding Co., China;

10. Mitsubishi Heavy Industries Ltd., Japan.

The features of a marketing policy of the shipyards of Republic of Korea are estimated in Allen Walker's report (Allen Walker, President, Shipbuilders Council of America) at the conference Shipbuilding Decisions ' 99 in 1999: South Korean shipbuilding pricing policies. Impact on the World shipbuilding market.

The report points, that from 1994 to 1996 the shipbuilding output in Republic of Korea has tripled.

During the period from 1997 to 1999 the prices for shipbuilding tonnage for a number of classes of cargo vessels at the shipyards of Republic of Korea were established below cost. For example, the average cost of built container vessels Panamax from 1997 to 1999 decreased almost by 30 %, bulk cargo vessels Panamax – by more than 30 %, container vessels with the capacity of 1100 TEU – by 15 %, bulk cargo vessels Capesize – by 22 %.

Dumping consequences in the Korean shipbuilding are estimated as by Council of ship builders of America dramatic. The share of the market of the Korean shipbuilding companies in sphere of container vessels output has increased from 15 % in 1997 to 70 % in 1999.

The similar economic policy during rather a long period is characteristic for the industry of East Asia states.

It should be noted, that before the Republic of Korea, Japan had a similar economic strategy after World War II in the commercial shipbuilding branch of industry, having superseding Great Britain from the first position.

The policy of international price competition is also typical for China in a broad industrial spectrum. In general, due to price competition, the industrially developed nations of East Asia support the positive export–import balance.

In order to hold back cheap imports and to increase export in other countries, such as in the USA and Russia can apply the depreciation of local currencies to stimulate exports as one of the measures, for example, such a measure can be a depreciation of dollar to keep the trade balance of the USA with China.

Probable consequences of such measures: reducing investment qualities of US dollar as a world reserve currency, the rising cost of energy, real estate, food products and others, the deterioration of macroeconomic indicators, and the specified effects may have a wave-like manner.

It may be noted that the characteristic national qualities of the Chinese, the Korean and the Japanese – hard work and discipline – open the competitive possibility of competition with the other states, influencing the global economic development.

Except the shipyards of the Republic of Korea the commercial shipbuilding is actively carried out by the Japanese shipbuilding companies among which are the following:

– Hakodate Shipyards, Hakodate Dock Co., Ltd., Hakodate;

– Hayashikane Yards, Shimonoseki;

– IHI Corporation, Marine United Inc., Tokyo Shipyard, Tokyo, AMTEC Aioi Shipyard;

– Imabari Shipbuilding Co., Ltd., Imabari yards, Imabari;

– Ishikawajima–Harima Heavy Industries (IHI) Co., Ltd., Tokyo;

– Kanda Yards, Kure;

– Kawasaki Heavy Industries, Ltd., Kawasaki Shipbuilding Corporation;

– Kochi Heavy Industries;

– Koyo Dockyard Co., Ltd., Koyo Yards, Mihara;

– Minami yard, Usuki;

– Mitsubishi Heavy Industries Yards, Shimonoseki, Nagasaki;

– Mitsui Engineering AND Shipbuilding Co., Ltd.;

– Naikai Zosen Yards;

– Namura Shipbuilding Co., Ltd.;

– Onomichi Dockyard Co., Ltd.;

– Oshima Shipbuilding Co., Ltd.;

– Sanoyas Hishino Meisho Corporation;

– Sasebo Heavy Industries Co., Ltd.;

– Shin Kurushima Dockyard Co., Ltd.;

– Sumitomo Heavy Industries, Ltd., Sumitomo Yards, Yokosuka;

– Toyohashi Shipbuilding Co., Ltd.;

– Tsuneishi Holdings Corporation;

– Universal Shipbuilding Corporation.

The Chinese shipbuilding companies united in the state corporation are also actively developing, for example:

– Chengxi Shipyard;

– Donghai Shipyard;

– Guangzhou Shipyard International Co., Ltd.;

– Guijiang Shipyard, Guangxi;

– Huangpu Shipyard, Guangzhou;

– Hudong Shipyard;

– Jiangnan Shipyard (Group) Co., Ltd.;

– Jiangxin Shipyard, Jiangxi;

– Jiangzhou Shipyard, Jiangxi;

– Qiuxin Shipyard;

– Shanghai Shipyard;

– Wenchong Shipyard, Guangzhou;

– Wuhu Shipyard;

– Xijiang Shipyard;

– Zhonghua Shipyard.

Besides the enterprises of East Asian region the influential shipbuilding companies and groups are:

1. A group of companies Aker Yards ASA, Oslo, Norway, the European group of companies in Norway, Germany, France, Finland, Romania, Ukraine with the separate enterprises in the South America (Brazil) and South East Asia (Vietnam), and Westamarin, Norway;

2. The German enterprises:

– Flensburger Schiffbau–Gesellschaft mbH & Co. KG, Flensburg;

– Lloyd Werft Bremerhaven GmbH, Bremerhaven;

– Schichau Seebeckwerft AG;

– Aker MTW Werft GmbH, Wismar;

– Aker Warnemunde Operations GmbH, Rostock–Warnemunde;

3. The Finnish enterprises:

– Wartsila Shipyard, Turku;

– Kvaerner Masa–Yards, Helsinki;

4. The Norwegian enterprises:

– A/S Fredriksstad mek. Verksted;

– Framn?s yards, Sandefjord;

– Fosen, Trondheim;

– Westamarin Building Yard.

A number of the shipbuilding companies productively operate in Great Britain, Sweden, France, Poland, Greece, Turkey, Croatia, Holland, Italy, Spain, the USA, Canada and Brazil, and also in Australia, Singapore, Vietnam, Malaysia and Indonesia.

The international specialization and cooperation are global factors of industrial development in modern shipbuilding and shipping.

The shipbuilding and shipping prospects should be predicted from positions of the investor, that is, subject of marine industrial activity and as general incentive motive to industrial development is an access of the investor to ocean resources.

The investor (in the aggregate of its qualities – interests, the rights and investment possibilities), as well as the marine environment, is an element of a complex into which marine engineering, the marine commercial vessels used by the investor to get an access to ocean resources, are also included.

In each separate case the complex in the specified structure is presented as the industrial enterprise, the part of the enterprise which can be estimated separately from other parts, or business of the several enterprises which part is the commercial vessel or some vessels.

Methodological importance of concepts «the marine company» or «property complex of the marine company’s real assets» is based on repeatability of properties of these objects, that is shipbuilding and shipping industries in separate states and in the world consist of the enterprises (operating property complexes), and repeated properties of the enterprises are transformed into properties of the industries, and the heart of each marine company is the complex including the investor with incentives to get an access to ocean resources, and the engineering, mostly marine vessels.

It makes sense the joint forecast of shipbuilding and shipping prospects, as the results of the forecast are presented in many respects by the general combination of indexes: characteristics of the shipyards correspond to characteristics of constructed batch commercial vessels, and intensity of shipbuilding and concentration of the capital, finally, are determined by shipping intensity. For the specified reason it is expedient to isolate methodologically shipbuilding and shipping as a single set in order to analyze of the general prospects.

The contemporary shipbuilding and shipping are developing in conditions of world political globalization. Basic similarity in understanding of the civil society order which is created in each separate state is characteristic. Due to this reason the political borders gradually lose their importance, the capital and labor can freely transfer, the international cooperation in separate industries and in groups of industries, in science and education is developing, and, finally the states unite in the political unions. Besides partial loss of importance of political borders in the process of globalization predicted for the XXI–st century, the general world political structure is changing.

In the geopolitical relation the global society gets multipolar structure (instead of borders there are centers and directions), that is, the centers of political system located, for example, in the North America, Europe and in East Asia are created. The centers of the political systems of a global society coincide with the centers of education, science and technologies.

During the previous historical period, including the XX–th century, there were general preconditions for formation of modern world shipbuilding and shipping structure by the beginning of present century. Preconditions can be characterized by the following factors:

– On the one hand, the greatest local concentration of the world capital in industries of commercial shipbuilding in East Asian countries – in Japan, in the Republic of Korea and in China, and also in European countries, but to a lesser extent than in East Asia, and export of the capital of the listed states to shipbuilding of other countries;

– On the other hand, the widespread distribution of the ocean resources developed mostly by industries of commercial shipping on the basis of operation of the real assets (marine vessels of different classes, fishing and others) constructed in the shipbuilding yards located in industrial centers.

And the commercial shipbuilding in East Asian countries and to a lesser extent in European countries is carried out mostly by a batch manufacturing on the basis of use of standard typical elements, and standardization is already provided at commercial vessel design stage. In other words, the modern commercial vessel is projected and made from standard typical elements.

It should be mentioned, that global distribution of ocean resources on the Earth, both with limits and outside of national jurisdictions of the majority of the states, does not coincide with the basic centers of world shipbuilding. The marine cargo traffics, the ocean biological resources, and also other resources of the ocean environment which are subject to development by industries of shipping, generally are outside the countries which carry out shipbuilding.

By the way, not all specified global centers of the modern industry are characterized by the developed commercial shipbuilding, but mostly the industrial centers in East Asia.

The basic marine cargo traffics are carried out from extensive territories in harbors of industrial centers in Europe, North America and East Asian industrial countries, having in mind cargo traffics of raw resources, and mainly the mineral oil which final users are located in industrial centers. Besides, transport cargo traffics are carried out between the ports located in global industrial centers.

Reverse cargo traffics (of resources and mineral oil) proportional in intensity in ports of departure are not provided, and from industrial centers cargo traffics in other industrial centers are made. In other words, after delivery of raw materials into the industrial centers the further freight traffic has «internal» charter between harbors of the industrial centers as the global markets of consumption geographically coincide with these industrial centers. Marine cargo traffics of goods between the industrial centers essentially are not so intensive, as cargo traffics of mineral resources and power resources from vast marine and coastal districts into the global centers.

It should be noted, that the main final geographical points for marine transportations are industrial centers and cargoes are collected mostly in these points, and points of departure are distributed everywhere.

The indexes of a cargo traffic capacity considering both the amount of cargo (by weight, by a cubic capacity, by number of places etc.), and distance, for example tonne–miles, etc. should be used as units of measuring the intensity of marine cargo shipping. When using similar indexes the cargo traffic capacity depends on the range of marine rout which can begin and in the main part pass outside the areas of global industrial centers.

On considered indexes of cargo traffic irrespectively of the amount of transported cargo intensive shipping in industrial centers is not provided, considering the limited range of the route within the occupied area, as industrial centers are placed locally. Thus, main sea cargo traffics are formed mainly outside of the global centers, but they are directed from the outside to these centers.

The shipping companies are inclined to be located geographically and nationally by the sources of cargo traffics. As sources of cargo traffics are located mostly outside the global centers, where shipbuilding industry is partially concentrated it is possible to view differences in respect of national identity of shipping and shipbuilding.

In particular, to locate the shipping companies the preference can be given geographically in so–called «offshore» zones, in the «convenient» countries and in those countries which possess ocean resources in abundance (countries which are sources of cargo traffics of mineral oil, are washed by the fishery seas, have a big length of a coastal line etc.), for example, in the countries Northern and the South America, in Russia, in Australia, in African countries. The listed states do not possess the developed commercial shipbuilding which level could be commensurated with shipbuilding manufacture in East Asian countries which do not have sufficient ocean resources.

In spite of the fact that most of population in East Asian countries lives in proximity to the ocean coasts, to a greater extent functions vitally thanks to the use of ocean resources (imported mineral oil extracted on the offshore in other countries, and national coastal fishery) and has the basic part of the world capital in commercial shipbuilding, it’s hardly possible to say, that East Asian countries are rich with ocean resources if to correlate the amount of national ocean resources with the population or with population density living in East Asia near coasts.

The basic areas of fishery in the World ocean are the Northern and the South America offshore (for example, Chile and USA offshore), the African offshore, the seas washing the north of Europe (Norway offshore), the seas washing the Russian east coast, and also open areas of the World ocean in geographical middle widths of Northern and Southern hemispheres where the plankton from equatorial areas is taken out by ocean currents (the districts of the pelagic fishery).

It’s clear, that the offshore and territorial waters of East Asian countries having the basic part of the world capital in commercial shipbuilding, although used quite intensively for the coastal fishery, they do not make the basic part of fishery grounds of the World ocean, proportional to a population of these countries and to a concentration of the capital in shipbuilding.

In other words, the basic sources of ocean biological resources to which in the national and geographical relation the marine industrial fishery gravitate are located outside the countries in which shipbuilding manufacture is concentrated, and it gives the basis to define the differences in respect of a national identity of fishery shipping and shipbuilding.

Ocean mineral deposits such as: stocks of hydrocarbonic raw materials on a offshore and mineral resources everywhere, including deep–water resources, can be referred to a number of basic objects of ocean resources which is the aim of investors activity and is a pricing basis in marine industrial activity. Besides, the basic objects are sea cargo traffics, almost half which, it is located between the Persian gulf and the Arabian peninsula offshore, on the one hand, and global industrial centers in the North America, Europe and East Asia, on the other hand, as well as ocean biological resources at coast and in geographical middle widths of oceans (fig. 18.3).

Fig. 18.3. Places of mineral deposits in the oceans:

![]() – rich deposits of ferro – manganese nodules;

– rich deposits of ferro – manganese nodules;

![]() – deposits of ferro – manganeze nodules average density;

– deposits of ferro – manganeze nodules average density;

![]() – phosphorite deposits;

– phosphorite deposits;

![]() – oil;

– oil;

![]() – gas hydrate;

– gas hydrate;

![]() – natural gas;

– natural gas;

![]() – metalliferous brine;

– metalliferous brine;

![]() – placer deposits of nonferrous and precious metals

– placer deposits of nonferrous and precious metals

The mineral deposits are located in the World Ocean outside the global centers of industry and shipbuilding and rather distantly.

The analogical conclusions concerning the industries of offshore development have no qualitative differences. The enterprises manufacturing of the marine engineering for development of oil and gas offshore resources are concentrated in global industrial centers, for example in the southeast of the USA – along the coast of the Gulf of Mexico, and the enterprises developing the offshore resources, besides the coast of the Gulf of Mexico are extensively distributed at the coasts of the seas, for example, washing Arabian peninsula, as well as an equatorial part of South America and Africa, Alaska, Sakhalin, the coast of the North Sea.

Note, that the development for defensive purposes of naval shipbuilding, with the general tonnage of the constructed ships by 1.5 % less than commercial shipbuilding (with the account tendencies of the further reduction of the tonnage in the naval shipbuilding), is more characteristic in the USA, Russia and in the states of European union, unlike the commercial shipbuilding which is carried out mainly in East Asia, and this fact is not negation of the general conclusions about national differences between shipping and shipbuilding, referring shipbuilding mostly to East Asian countries, and shipping – to the countries, including industrialized ones, among those which possess ocean resources.

It is the development of naval shipbuilding and shipping to control the ocean resources in these countries, which less intensive than in East Asia commercial shipbuilding that supports the general conclusions about non–uniform distribution of ocean resources and capitals of shipbuilding industries by the national identity.

It should be noted, that in early XXI–st century due to a non–uniformity of distribution of shipbuilding and shipping there are no countries «self–sufficient» in these industries, that is such which commercial shipbuilding could completely satisfy the needs of shipping in domestic market and would not be export-oriented, there are no separate countries, that can develop modern shipbuilding and shipping separately from other countries, and the international cooperation is required, and the specified circumstance is the global factor of industrial development in shipbuilding and shipping.

Large-scale objects of the further and prospective development are the Arctic seas and the Southern ocean washing Antarctica. And motives of the polar seas development have basically global character.

There are no separate states interested in investing in polar shipping in areas with low density of population in the general territories, considering, that ability to live in these areas can be first of all a subject of international interests and should be carried out mainly on the basis of the international investments, instead of at the expense of separate countries.

Otherwise, that is in case of independent national investment by separate countries in polar shipping, other states which did not participate in investing, cannot be admitted to results of the development of the Arctic seas and Southern ocean in a corresponding part that will hamper both the development of the polar seas and coasts and the development of international cooperation in shipbuilding and shipping.

Thus, in the early XXI–st century the possibilities of national development of shipbuilding and shipping are generally exhausted and the international cooperation is the global factor of prospective development.

The international cooperation makes appreciable impact on stages of commercial vessel manufacturing, including designing, productive operation and even utilization.

Test questions

1. Causes of the growth of prices for shipbuilding production of the second hand market marine commercial vessels.

2. Global distribution of shipbuilding manufacturing output in relation to the national factor.

3. Features of a marketing policy of the South Korean’s shipbuilding companies.

4. International specialization and cooperation as global factors of industrial development in modern shipbuilding and shipping.

5. Geographical localization of shipping companies in «offshore» territories and in those countries which possess marine wealth in abundance.

6. Geography of ocean mineral deposits.

18.2. Investor as a subject of the economic interests in marine industrial activity and the property rights

Generally the investment project is not carried out by one legal entity, and there is a set of interested parties. Construction and productive operation of marine vessels or other assets of the marine company is characterized by capital intensity, planned for the long period, involves to commercial risks, and carried out usually by several participants who are independent investors uniting by the terms of contracts.(18) |

Test questions

1. Structure of the Investor (the participants of the Parties) of the marine industrial activity and necessity of investment risks minimization.

2. National identity of the Ship–owner and the Charterer (in the Investor structure, with the account the Creditor opinion).

3. Expediency of the investment loan for the efficiency of the Investor.

4. Advantages of commercial shipbuilding at the shipyards of East Asian countries.

5. Sequence of investment stages since the formation of the Investor structure.

6. Characteristic risks in case of manufacture of a batch vessel and in case of vessel purchase at the second hand market.

7. Determination «losses estimated in advance» in the contract of vessel manufacturing.

8. Proportional parity of private and extra financing with the account the average weighed value of the capital.

9. Examples of the large financial institutions which fulfill the vessel construction and shipping crediting.

10. Criteria of estimation of a borrower by the credit institution.

18.3. Value and investments efficiency estimation of the marine object as a separate entity

The estimation of economic efficiency of marine object (the property complex, the commercial vessel or the asset) is possible, if the object is isolated, that is, if the marches, the object set and structure are defined.

Determination of the boundaries of the object is included into a number of system requirements and allows establishing of the external data list – characteristics of the environment of the object and characteristics of the interacting objects.

Isolation of the marine commercial vessel, that is, a possibility to evaluate vessel as a working enterprise, usually means necessity to consider the adjustment corresponding to working assets since the vessel should be equipped for the voyage, that is, the isolated object acting as an enterprise or a property complex can be an equipped vessel as a whole with working assets.

Isolation of the marine object is an integral precondition for the evaluation and investments efficiency estimation and means the following:

– Financial and property flows through the boundaries of the object of evaluation can be made only on the basis of civil–law contracts;

– Concerning the isolated object of evaluation the financial records are kept (or can be conducted);

– Financing sources are with in the isolated object of evaluation; if extra financing is used it is provided with liquidity of assets in object and cannot exceed liquid pledge; there are no sources of financing outside of the evaluated object, directed to object which would not be paid at the expense of the resources of the evaluated object;

– The financial result is formed within the isolated object of evaluation and distributed for its development in interests of the investor; there is no financing outside the boundaries of the object of evaluation in other interests;

– Concerning the isolated marine object it is possible to determine the rights of the investor – the physical or legal entity interested in increase of the value of the project (standard motivation of the investor).

While determining the boundaries of the object the part of the assets (a property complex), which within the limits of certain assumptions about the evaluation and efficiency estimation of investments from the economic point of view can be considered irrespective of other part of property, should be selected.

The isolated marine object – the commercial vessel, the property complex or the marine company as a whole, as a typical assumption in applied expert studying, is evaluated separately from other property (assets).

Other property is considered as a means of additional security (guarantees) in the course of the investment activity directed for fleet renovation, branch activity (transport, fishery or other shipping) and financial activity of a profit capitalization in the course of branch and investment activity which is used further for investment activity, that in aggregate with replenishment of resource base – with development of cargo traffics or quotas for ocean biological resources development – leads to maximisation of the property complex value.

The models of the evaluation and efficiency estimation of investments into real assets of the marine company – in fleet renovation and replenishmrnt – is carried out with the account financial constrain of the investor. Within the limits of financial constrain it is supposed, that any investments from the outside are not received, except accumulation of the profit within the limits of the isolated object of evaluation in the process of fulfillment of branch activity and investment activity.

Besides, within the limits of financial constrain it is supposed, that financial assets are not spent over the limits of the isolated object of evaluation – an asset or a property complex, and capitalized in the monetary form for investing in object.

To estimate financial constrain real assets should be evaluated as a part of the property complex. It should be taken into consideration, that if extra financing are used for fleet renovation and replenishment, then the loan is determined with the account the value of assets in the pledge as a part of the property complex, or with the account the factor of a cash flow according to property complex estimation, i.e. also in interrelation with the assets value.

So the use of the loan for fleet renovation and replenishment is not a negation of financial constrain of the investor which is an important methodological precondition for investment planning, and prospective extra financial assets, with the account the liquidity of the loan, are proportional to the value of assets collected earlier as a part of the property complex of the marine company.

Test questions

1. Determination of the boundaries delimitation of the evaluated object as a system precondition of the evaluation and economical efficiency estimation.

2. Isolation of the commercial vessel as an object of an evaluation when making adjustment to the working assets value.

3. Conditions of the economic isolation of the object of evaluation.

4. The limitations of the commercial vessel value and efficiency estimation and replacement of the rest part of the property complex with the adjustment to vessel evaluation.

5. The financial constrain of the investor in the process of investments planning (when estimating the value and efficiency).