20. Evaluation of ocean resources and unidentifiable intangible asset taking into account of investment risks in marine industrial activity

Marine wealth in methodological sense is any useful properties of the marine environment for which development the investor aims his interests and activity. In applied tasks the ocean resources can be evaluated, for example, by estimating of fishery quotas for ocean biological resources development, or by evaluating of the advantages of access to marine cargo traffics, etc. And the concept of marine environment means not only the physical water environment, but the ocean as a reservoir having the characteristics of a geographical location, climatic conditions, biological resources, minerals of ocean bottom, industrial potential of coasts and other characteristics which corresponds to economic or other interests of the investor in marine environment, besides, it is characterized by the intensity of marine cargo transportations.

20.1. Evaluation of marine resources and unidentifiable intangible asset of a marine company with the account of total risks of innovative strategy

While estimating the marine company’s property complex the estimation of the ocean resources means mostly the estimation of the goodwill – the grouped unidentifiable intangible asset which characterizes the advantages of investor’s access to marine wealth and based on the concepts of the superfluous income and residual value. And, unlike widespread definition of goodwill as tendencies of clients to use again the same company, that is, as the evaluation of the demand for resources, at the basis for the estimation of the ocean resources value is the estimation of the supply from the point of demand in the marine industrial activity.

Not only in the field of marine activity, but also in other areas can the goodwill be a result of possible advantages of the investor’s access to resources. In particular, when investing in the real estate the goodwill is closely connected with the investor’s advantages in access to acquisition of the property or in using the sites for construction.

In order of the real estate rent for the investing or in case of the land plot rent for real estate constructing the goodwill can be the result of investor’s access for the available advantages of economy of the rent charges.

The interrelation of the goodwill and the natural wealth can be explained by an example of real estate evaluation, considering, that in case of real estate construction the territory occupied for construction is natural resource, characterized by the location, the area, the form, the orientation etc. When the real estate is situated in a busy place the advantages can be estimated either as the goodwill of the company using real estate in a busy place and adherence of the clientele, or as advantages in the value of the real estate located at an expensive site of busy territory.

The definition of an asset as goodwill or as marine wealth to which development the investments into real assets are made and the property complex of the marine company is formed, depends on context.

In order to estimate the marine company’s property complex value the unidentifiable intangible asset – goodwill should be determined. When evaluating of the isolated real asset (or commercial vessel) of the marine company’s property complex there is a task to estimate the influence of the marine environment productivity on the asset value.

Unidentifiable intangible asset (goodwill) corresponds to a difference between the value property of the company’s complex value and the total sum of values of real assets taken separately, including identified intangible assets as well as financial assets.

The goodwill value of the marine company can correspond to the residue of:

– Total sum of values of intangible assets after deducting it the values of all identified intangible assets;

– Total values of the marine company’s property complex after deducting the values of the material assets, including financial and identified intangible;

– Present value of superfluous profit cash flow over the general profit of the marine company identified assets, including the profit of the identified intangible assets.

In respect of economic methodology the activity of investors and the managers serving interests of investors is directed to the increase of the marine company’s property complex value by production the unidentifiable intangible asset.

The definition is fully fair for new enterprises at an innovative stage of their development when the profit is not alienated as a financial asset, but re–invested in real assets, including intangible ones, bought as the intellectual property or the equal rights.

The growth of the property complex by the value of unidentifiable intangible asset just encourages the investor to create of the marine company or enterprise division as combinations of the real assets paid while investing by financial assets.

At the same time investing in the financial assets can serve as a way of capitalization for the subsequent capital financing in real assets.

The goodwill is an unidentifiable intangible asset, that is the commercial advantages of the marine company which in real assets don’t have it taken separately, including material assets for example marine commercial vessels and identified intangible assets.

In figurative definition the property rights underlying the unidentifiable intangible asset – goodwill, are equal to a difference between:

– Property rights (possession, use and disposal, under article 209 of the Civil code of Russian Federation) concerning the property complex (on article 132 of the Civil code, part 2), taken as a whole;

– And, the property rights concerning all isolated real assets, including identified intangible assets (intellectual property and equivalent rights under article 138 of the Civil code of Russian Federation), in the sum with financial assets.

Some difficulty in understanding can arise in connection with measurement of the amount of the ocean resources as, in particular, in case of real estate evaluation the natural resources – built–up land plots – are quite measurable and there is a system of property rights registration unlike in the field of the marine industrial activity.

Without going into details the measurement of the ocean resources by characteristics of those marine engineering and ocean technology, which are used for the development of these resources, can be recommended as a general concept. For example, it is possible to measure marine cargo traffic in units of cargo vessel carrying capacity or in number of necessary cargo vessels with the account their carrying capacity. Also it is possible to measure ocean biological resources by the productivity of fishing vessels. The coastal ship–repair infrastructure can be characterized by the number of vessels, undergoing repair and maintenance service etc.

There is also the task of protection of the investor’s interests in the sphere of marine industrial activity. This protection in real estate building industry would be done on the basis of marking of the territories.

One shouldn’t think that the innovative strategy aimed at the growth of the value of the marine company’s property complex by investing in real assets, by forming the property complex structure and providing of the access to marine wealth is not protected from an un–authorized use.

A certain restriction of access is the condition of financial sufficiency of means of investing in real assets, that is, the realization of innovative strategy of the investor should be unavailable without sufficient financing.

On the other hand, excessive financial capacity can be an obstacle for the realization of innovative strategy too, since they give the investor the opportunity for more expensive strategy.

From the system point of view to evaluate the unidentifiable intangible asset while estimating the property complex (or to evaluate of the ocean resources while estimating the isolated asset, for example a vessel) it is necessary to consider the sequence of investor actions during the period

t-t0 of investing in the formation of the structure of the real assets property complex:

– The acquisition of tangible and identified intangible assets with the total value

which in a certain structure and in the aggregate are the property complex of the marine company;

– Sale by the value

MV of tangible and identified intangible assets, which for the unidentifiable intangible asset

MW are more expensive in aggregate than separately that the reason why the real assets had been bought separately to be sold in aggregate (namely in order of estimation of the isolated asset of the marine company the set is the asset and the marine wealth taken together);

– Cyclic repetition of the specified actions with period

.

And the difference of the same property value separately and in aggregate, allowing to use the set of property as a business based on the concepts of loyalty of clientele, the superfluous income and residual value, is unidentifiable intangible asset – goodwill – according to

MW=MV-MVΣ=NPVΣ .

Unidentifiable intangible asset

MW is equal to the net present value of the marine company’s property complex

MW=NPVΣ from the methodological point of view and means an evaluation of the ocean resources, that is an estimation of set of technological, legal and other possibilities of the ocean resources (marine wealth) development.

In correlation with the isolated real asset of the marine company, the index

MWn means the estimation of the ocean resources contribution associated with this asset, by the value of this asset and is equal to the net present value

MWn=

NPVn of the marine company real asset, and in the sum with the value of asset

MVn+MWn methodologically means the investment value of the asset.

According to the discount formula of the present value the capitalization of the marine company’s property complex assets is determined as

, ,

|

(20.1) |

where

– the duration of the period of structurization (regulation) of set of real assets when investing financial assets, in particular, the duration of creation of the marine company’s property complex and the goodwill or the property complex in the structure of the enterprise, and also, the duration of manufacture of an asset, for example, the construction of the vessel;

i is the index of additional net values as the discounting rate, corresponding also to the interest rate in a certain economic sector with the duration of assets structurization

.

From the system point of view the duration of the marine company’s property complex creation or the constructing of the isolated real asset, is an indicator of recurrence (repeatability) and should be estimated from the point of view of financial capacity and economic feasibility.

The duration of the period of the property complex creation or period of the constructing of the isolated real asset of marine company

is not related to the payback period or to the calendar periodicity.

From the investor’s point of view the duration of the period

corresponds to its financial capacity and an of the value

MV-MVΣ to the investment

MVΣ , and also to total sum of the risks of innovative strategy

i.

After mathematical transformations of the formula (20.1) the duration of the period of creation of the marine company’s property complex (or manufacturing of the isolated real asset) from the point of view of the financial capacity of the investor characterized by his initial investments

MVΣ , can be estimated, as:

, or  |

(20.2) |

For an economic environment the estimation of the duration of the period

t-t0 of the property complex creation or the period of the construction of the isolated real asset of the marine company is an object – matter of economic feasibility and there are alternatives. Depending on concentration of industrial capacity the duration of the period

can be various and there is a redistribution of industrial capacity within an economic environment for increase of their cumulative efficiency.

Since the duration of the period

, which is required for generating the additional net value, is various in different sectors of economy, as well as an for progress of additional net values according to the discounting rate

i it is possible to speak about the dependence between the duration of structurization of assets

t-t0 and the sum of risks

i depending on industrial branch.

From the formal point the unidentifiable intangible asset – goodwill – corresponds to an increment of the present value of the marine company’s property complex in relation to the total value of investments when arranging commercial ordering real assets in the set and characterizes the ability of the property complex to increase the present value during its formation. Therefore it is important to have an approach used in estimation of the period duration

which is required for generating the additional net value that is considered in details in the following article 20.2.

The evaluation of unidentifiable intangible asset of the marine company

MW, that is, the evaluation of the increment of the property complex value corresponds with mathematical derivative of the dependence of the marine company value on time

MV created while investing financial assets in real – tangible and identified intangible assets which total cost is equal

, that is

, ,

|

(20.3) |

where

– the increment of the value during the period

of formation of the property complex.

As the marine company’s property complex value capitalized in accordance with the formula (20.1) is equal

, it is possible to transform the formula (20.3) as

MW=MV×ln(1+i)×(t-t0) . |

(20.4) |

The dependence by the formula (20.3) of the ratio of the marine company unidentifiable intangible asset

MW to the value of the invested real assets on the index of commercial risk as the discounting rate

i and on the duration (period) of assets structurization in the property complex

is shown on the graph (fig. 20.1).

Thus, by the relative value the unidentifiable intangible asset of the marine company essentially depends on the discounting rate and there is a relation between the factors of loyalty of clientele, the income superfluous and residual value, which mean also the efficiency of the ocean resources, and its positive influence on the value of the isolated asset of the marine company, on the one hand, and the indicators of the commercial risk on the other hand which at the same time is connected with predicted economic efficiency.

According the drawing (fig. 20.1) it is clear, that the more proportional share of unidentifiable intangible asset – goodwill – as a part of the marine company’s property complex value (or the estimation of the ocean resources relative value, associable with the isolated asset), the more the index of commercial risk.

Since, on the other hand, the marine company’s property complex value with certain assumptions can be calculated by the formula

, the value of unidentifiable intangible asset

MW (or marine wealth) is related to the estimation of the cash flow

NOI, as

MW=NOI×ln(1+i)/i×(t-t0), |

(20.5) |

or the use of discounting by the Euler’ number exponential function by the factor

for evaluation of unidentifiable intangible asset

MW of the marine company depending on the net operating income leads to calculation by formula

MW=NOI×i/(ei-1

)×(t-t0) , which can be recommended as a variant of the formula (20.5).

Besides using the formulas (20.3, 20.4, 20.5) taking into account the time of completion of the formation and the time of input of the marine company’s property complex (or the isolated real asset in its structure) with little commercial risks when

ln(1

+i)≈(ei-1

)≈i the additional approximate formulas for the estimation of unidentifiable intangible asset of the marine company, that is, for estimation of the ocean resources are the following:

, or , or  , ,

|

(20.6) |

and also MW≈MV×i×(t-t0) and MW≈NOI×(t-t0) . |

(20.6 and 20.7) |

With rather short duration

t-t0 of the investment in creation of the marine company’s property complex structure, that is, provided that

the approximate value estimation of unidentifiable intangible asset

MW, that is, the evaluation of the ocean resources, is equal

| MW ≈MVΣ×(i×(t-t0))2. |

(20.8) |

Test questions

1. Concept of group unidentifiable intangible asset – goodwill – as a part of the marine company’s property complex.

2. Goodwill sources.

3. Concepts of goodwill definition.

4. Incentives of the investor to buy marine company’s real assets.

5. Financial protection of the investor intellectual activity.

6. Methodological conformity of the property rights underlying unidentifiable intangible asset – goodwill.

7. Systematic approach in the basis of the sequence of the investor’s actions to determine the unidentifiable intangible asset.

8. Value of the assets capitalization by the discount formula of present value.

9. Formal–logic sense of estimation of the unidentifiable intangible asset.

10. Dependence of the goodwill on the total value of invested real assets and the commercial risks index as the discounting rate (the formula derivation).

11. Main parties participating in intangible assets generation.

12. An evaluation of advantages of the access to marine wealth as unidentifiable intangible asset – goodwill – of the marine company and as a contribution of the ocean resources to the value of the isolated real asset.

13. Interrelation of the marine wealth evaluation, the unidentifiable intangible asset and the discounting rate index of the commercial risk.

14. Ocean resources evaluation with the account total investments into the real asset and the discounting rate index of the commercial risk.

15. Approximate estimation of the ocean resources taking into account methodological assumptions (the formula derivation).

16. Based on the conformity of discounting by the arithmetic discount financial functions and using the exponential functions of the Euler’ number formal sign that the commercial risks are little.

17. Methodological conformity of the ocean resources estimation and the net present value.

18. Estimation of a reference point of the ocean resources value from the point of view of the investor who is consistently manufactures the assets and sells them, for example the marine company’s property complex creation and sale, as a systematic activity.

20.2. Evaluation of ocean resources and goodwill with the account of balance of real assets structure of the marine company

The value of the ocean resources which makes sense only in a context of a set of technological, legal and other opportunities of their development should be correlated with the unidentifiable intangible asset – goodwill of the marine company with its net present value. Thus marine wealth in the methodological relation is any useful properties of the marine environment for which development the investor’s activity is directed, among them we evaluate not only physical properties of the water environment, but also the sea, as a reservoir with the account the size, geographical and climatic characteristics, activity developments in the ocean and at coasts, economic potential of marine cargo transportations, stocks of ocean biological resources, ocean–bottom minerals at shelf and behind its limits, resources of marine power, recreational possibilities etc.

On the one hand, the account of the invested assets and risks of innovative strategy (article 20.1) is the precondition for an estimation of the ocean resources – the evaluation of unidentifiable intangible asset of the marine company. On the other hand, the evaluation of unidentifiable intangible asset, which manufacture is the purpose of innovative strategy and investment of financial assets in formation of the real assets of the marine company’s property complex structure, can be made on the basis of the analysis of both the balance of real assets and stability of balance structure.

Thus, the unidentifiable intangible asset corresponding to an evaluation of the ocean resources is the characteristic of stability of the balance assets in the structure of the marine company’s property complex and the purpose of investing financial assets in formation of the structure of the property complex of its real assets.

The equation of the balance of the assets in the structure of the marine company’s property complex looks like:

, or |

(20.9) |

, ,

|

(20.10) |

where

– the goodwill as the net present value of the marine company’s property complex, corresponding to the evaluation of the ocean resources

MW,

NPVn – the net present value

n– th asset as a part of its investment value

MVn+NPVn,

MV – the marine company’s property complex value,

MVn – the value of isolated

n– th asset of the property complex,

MVΣ – the total value of the tangible and identified intangible assets which in aggregate are the property complex of the marine company, the investment at formation of the property complex is

.

Differentiating the formula (20.10) it is possible to obtain the assets structure balance equation of the marine company’s property complex as increments:

, further

,

or after the mathematical transformations

and and  , ,

|

(20.11) |

where

– the factor of the net present value characterizing the relation of an increment of the total sum of the net present value

of the marine company’s property complex to a total increment of the invested value – the sums of the net present value of separate assets

.

In other words, the net present value factor

is the proportional relation between an increment of the «whole» – the net present value of the marine company’s property complex and a total increment of «parts» – the costs of separate assets.

If in case of combination of parts, real assets of the marine company, in a structure of the property complex the additional net value doesn’t arise, for example because of a strategic error or excessive risks the net present value factor is equal to a one

=1. Thus there are no economic reasons for stability, or, in other words, the reason for the balance of the structure of the property complex. Such reason could appear when in case of combination of the parts in an integral structure the arising additional net value is not equal to zero, and the net present value factor is larger than a one.

That is, the balance equation of the marine company’s property complex structure of assets can be presented in a differential form depending on the total sum of increments

of the invested value, as:

, ,

|

(20.12) |

and, the increments of the invested value

are formed of the profit or the savings distributed in profit.

The basis for use of the balance equation in the differential form (20.12) assets in the structure of the marine company’s property complex is the following economic definition: an unidentifiable intangible asset corresponds to an increment of the net present value by an increment of the invested value.

The system concept of continuity is that the investments are not carried out from zero, and are a continuation of previous investments – capitalization for the initial capital. The continuity concept means the evaluation of the present solvency of the investor, since the further investments are considered as continuation.

It should be noted, that the conclusion of formulas (20.1, 20.3 – 20.7, article 20.1) also is more correct in increments with the account the system concept of economic continuity. For this purpose it should be required to formulate the precondition of the formula (20.1) in increments

as:

, and also to transform the resulting formula (20.3 – 20.7).

However, in view of methodology the substantiation of the specified formulas in article 20.1 is made not in increments, but in final values, since there is a subject of the ocean resources evaluation and the unidentifiable intangible asset – goodwill of the marine company depending on the total commercial risks index for the set duration of the property complex formation, instead of on the basis of the assets structure stability balance analysis, including, the balance of the accumulated (capitalized) assets and increments that is done below.

A continuity concept can be illustrated additionally by determining the of economic criterion of investments profitability which is sometimes defined as a relation of the profit to the investments, but corresponds more precisely to the relation of the increment of the profit to the increment of the investments causing this increase in profits, that in a limit (at a level of little increments) means mathematical derivative of the profit of investments.

The stability of assets structure balance in the property complex means the dependence of the summands of the net present value

NPVn , referred to the isolated assets, on the net present value of the marine company’s property complex

, for example a proportional dependence

.

The assets structure balance would be unstable, if the summands of the net present value

were independent on the total net present value of the property complex

, that is

.

Other dependence instead of proportional to one or another degree of total net present value

, is generally possible for each of addends of the net present value

, referred to the isolated assets.

If to remain within the limits of an assumption that the addends of the equation of balance (20.10) of marine company’s property complex assets according to stability are included into one of two groups: either proportionally dependent on the total net present value of the property complex or independent on the total net present value this equation becomes:

, ,

|

(20.13) |

where

N1 – the group of assets in proportional dependence

of the net present value referred to the isolated asset, on the net present value of complex

,

– the group of assets independent on the property complex according to the net present value

.

The factor of balance

of assets structure of the property complex can be defined as a relation of a total sum of estimation of addends of the net present value

, referred to the isolated assets, consisting in proportional dependence on one or another degree of the net present value of the marine company’s property complex

to the net present value of the property complex, as:

, ,

|

(20.14) |

Within the limits of a used assumption that the addends of equations (20.7) according to stability of the balance of the assets structure and the marine company structure enter into one of two groups: addends proportionally dependent on the net present value of the property complex and independent on the total net present value, the net present value factor

fNPV

, determined by the formula (20.11), is equal

, and  . |

(20.15) |

On the other hand, with rather short duration

t-t0 of the period of investing in creation of the structure of the marine company’s property complex (with the account assumptions, see article 20.1) the approximate value estimation of unidentifiable intangible asset

MW, that is the evaluation of the ocean resources by the formula

, and with the account the conformity of economic indexes at the level of increments and replacements of designations in the formula (20.8):

MW~ΔNPVΣ and

the evaluation of the ocean resources depending on the duration of the period of investing and risks evaluation is:

. |

(20.16) |

Equating the right parts of the formulas (20.15) and (20.16) and after mathematical transformations with the account the considered assumptions the period of duration of formation of the marine company’s property complex

with the account total commercial risks and also the factor

of the assets structure balance in the property complex, can be determined as:

. .

|

(20.17) |

The duration of the marine company’s property complex formation

, estimated by the approximate formula (20.17), corresponds to the joint account of the following preconditions:

– Dependences of unidentifiable intangible asset which means the evaluation of the ocean resources, on the estimation of the commercial risks with the account variable duration of marine company formation (article 20.1);

– Determination of the unidentifiable intangible asset of the marine company with the account the factor of the present value, characterising the balance stability of the marine company in a proportion of its net present value, that is, unidentifiable intangible asset – estimation of the ocean resources to the total invested assets.

The dependence of the duration of the property complex formation

on the basic influencing factors, is shown on the figure 20.2 which corresponds to the formula (20.17) with the account the used assumptions and preconditions.

Figure 20.2 shows, that the index of total commercial risks according to the discounting rate makes more substantial impact on the duration of the period of the marine company’s property complex formation, than factor

of the assets structure balance in the property complex, and in the most general approach the duration of the marine company’s property complex formation is proportional to the investments payback period, that is

~

~

TR = 1/

IRR.

To the net present value factor

, used for the evaluation of unidentifiable intangible asset of the marine company, earlier there was the assumption is, that the addends of the balance equation enter into one of two groups: either proportionally dependent on the total net present value of the property complex or independent of the total net present value, and the factor of balance

of assets structure in the property complex is defined as a relation of its total sum of estimations the net present value of the marine company’s property complex

in linear proportional dependence.

It should be noted, that the determination of the net present value factor  by the formula (20.11) is the common solution and is not necessarily connected with the specified assumption. To explain this fact it makes sense to consider the following example. If the general set of the marine company’s property complex assets can be presented not by the formula (20.13), but as a part of the following groups where: N1 – the group of assets in linear proportional dependence on the total net present value

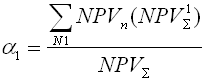

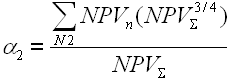

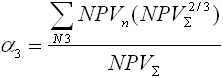

by the formula (20.11) is the common solution and is not necessarily connected with the specified assumption. To explain this fact it makes sense to consider the following example. If the general set of the marine company’s property complex assets can be presented not by the formula (20.13), but as a part of the following groups where: N1 – the group of assets in linear proportional dependence on the total net present value  , N2– the group of assets in a proportion of degree 3/4 from total net present value

, N2– the group of assets in a proportion of degree 3/4 from total net present value  , N3 – the group of assets in a proportion of degree 2/3 from total net present value

, N3 – the group of assets in a proportion of degree 2/3 from total net present value  , N4 – the group of assets in a proportion of degree 1/2 from the total net present value

, N4 – the group of assets in a proportion of degree 1/2 from the total net present value  and (N – N1 – N2 – N3 – N4 ) – the group of assets independent on the total net present value

and (N – N1 – N2 – N3 – N4 ) – the group of assets independent on the total net present value  , then the net present value factor is determined with the account a mathematical derivative by the formula (20.11) as:

, then the net present value factor is determined with the account a mathematical derivative by the formula (20.11) as:

, and using symbols:

, and using symbols:

,

,

,

,

the net present value factor

can be determined, as:

, besides, for the considered example it is also possible, to determine the general factor

of the assets structure balance in the marine company’s property complex by the formula

, ,

|

(20.18) |

and, factors

,

,

,

in the considered example show, what part of the total net present value

of the marine company’s property complex is the addends associable with the separate isolated assets and correlated with total net present value in a proportion of its certain degree serving in mathematical differentiation as a multiplier for determination of the net present value factor

, and this rule can be extended for the addends in another degree of proportional dependence on the total net present value

.

If to admit, also, that the net present value

of the marine company’s property complex is distributed between separate assets proportionally to their own market value, the factors

,

,

,

can be determined in the proportion of the market value

by the groups of assets in the property complex, as:

,

,

,

, that is

,

and thus it is possible to use the data of the marine company, for example, by the tables of the accounting balance corrected for market prices.

When there is no other opportunities the factor

of assets structure balance of the marine company’s property complex, apparently, should be evaluated expertly, probably on the basis of estimations of the balance, unidentifiable intangible asset and marine wealth by the data of the property complex of other marine enterprises similar to some extent with the account the analysis of similarity and comparability by the economic and the industrial indicators.

Coming back from evaluations of the economic indexes increments to the indexes in their final form and keeping in mind, that in any case the values are increments to previous values according to the system concept of continuity, the equation of assets structure balance (20.11) in the assumption about distribution of the net present value of the marine company between the isolated assets proportionally to their market evaluation becomes:

and  . |

(20.19) |

The formulas (20.11 and 20.12) of the ocean resources evaluation

MW – goodwill

of the marine company show, that the goodwill evaluation to the invested assets is proportional to the net present value factor and, with the account of the stability of assets structure balance as a part of the marine company’s property complex, can be determined approximately, as:

. .

|

(20.20) |

Test questions

1. Marine wealth as properties of the marine environment useful for the investor.

2. Interrelation of the economic concepts: the goodwill of the marine company, the net present value of its property complex and the ocean resources.

3. Bilateral preconditions for the ocean resources evaluation – definitions of the marine company unidentifiable intangible asset value.

4. Characteristic of stability of the marine company assets structure.

5. Equation of assets balance in the structure of the marine company’s property complex (two forms).

6. Differential form of equation of the marine company assets balance structure.

7. Economic sense of the net present value factor as a stability characteristic – the balance of the property complex structure.

8. Intangible asset at an increment of the invested costs.

9. Systematic concept of investments continuity and the evaluation of the investor current solvency.

10. Stability of the assets structure balance in the property complex.

11. Equation of assets structure balance of the marine company’s property complex in an assumption about proportionality of addends of one degree or another of the net present value.

12. The factor of assets structure balance of the marine company’s property complex.

13. Estimation of the net present value factor depending on the factor of assets structure balance.

14. Estimation of the duration of the marine company’s property complex formation, the approximate estimation of the duration of the property complex formation.

15. Estimation of the net present value factor with the account diverse character of the proportional dependences of addends of the balance equations.

16. General formula of the estimation of the factor of the marine company’s property complex assets structure.

17. The assumption about distribution of the marine company net present value proportionally to the market evaluation of the isolated assets and the equation of assets structure balance in this assumption.